Budgeting Tips for Beginners

*This post may contain affiliate links. See disclosure for more information

Budgeting Tips for Beginners: How to Budget in 2023

The easiest way to make a monthly budget is to add up your monthly wants and needs, subtract them from your income, and save the rest. Why then, do so many of us fail at budgeting? Probably because many of us never learned these budgeting tips for beginners.

The Great Recession of 2007 was a wake-up call for our family. By the end of 2007, we were well over $130,000 in debt and living paycheck to paycheck on just over $40,000 a year for a family of five. We needed a crash course in budgeting, fast!

The fact is, it took me years to figure out how to create a budget for our family (I’m a slow learner). And even longer to learn how to live a frugal lifestyle.

Eventually, I learned to embrace budgeting because of the freedom it provides.

Since I (finally) learned to love budgeting, my husband and I have paid off hundreds of thousands of dollars in debt and fully-funded our emergency savings.

All this while continuing to live a beautiful life (on a budget, of course)!

Did you know two-thirds of Americans fail to budget each month? Let’s change that statistic, shall we?

What’s the purpose of budgeting tips for beginners?

A budget is simply a plan for telling your money where to go. In his book, The Total Money Makeover, Dave Ramsey calls it ‘Giving every dollar a name’, or a specific job to do each month.

Creating a budget doesn’t mean you wave a magic wand and all your money dreams come true. But, it is a step in the right financial direction.

There’s no one right way to budget. It’s called ‘personal’ finance for a reason.

Who should use a budget? EVERYONE! Whether you make $4,700, $47,000, or $470,000 per year, you should learn how to create (and live on) a budget. It’s never too late to start!

Budgeting tips for beginners: Why you need a budget

Without a budget, you are failing to plan, which means you are planning to fail.

The number one reason most budgets fail is because people view them as a prison. In reality, the opposite is true; living on a budget sets you free from the paycheck to paycheck cycle!

I’m not gonna lie, budgeting takes some getting used to. Especially if you’re a “free spirit” like me. You don’t let people tell you what to do, so you’re certainly not going to let a piece of paper with some numbers on it boss you around!

Until that is, you accidentally overdraw your bank account. Or, you coast into the gas station on fumes only to discover you don’t have enough money to fill up your gas tank!

Yep, sooner or later, the day will come when you discover the real reasons behind why you need a budget.

The top three reasons you need a budget are:

- Living on a budget puts you in charge of your money

- Having a budget helps you live on less than you earn (which allows you to build wealth)

- Sticking to a budget can help you get out of debt faster

Budgeting tips for Beginners: Methods For Budgeting

Budgeting is the process of planning and allocating financial resources to achieve one’s goals. A budget can help you manage your expenses, reduce debt, save for emergencies and future needs, and achieve your financial goals.

There are several methods for budgeting, each with its own advantages and disadvantages. Here are some of the most common budgeting methods:

Zero-Sum Budget

A zero-sum budget is where you assign every dollar of your income to a specific category. This budgeting method can help you maximize your income by ensuring that every dollar is used effectively.

Basically, it involves tracking all expenses and income sources, including rental income, student loan payments, utility bills, and unexpected expenses.

To create a zero-sum budget, start by determining your sources of income and listing your expenses. Then, divide your expenses into categories such as housing, transportation, food, and entertainment.

After that, you will then allocate your income to each category based on your spending habits, budgeting goals, and financial priorities. If you have money left over, put it into savings or pay down debt.

Cash-Based Budget

A cash-based budget is a simple and effective way to manage your finances.

It involves using cash to pay for all your expenses, which can help you avoid overspending and stay within your means. By only spending the cash you have on hand, you can avoid the temptation to rely on credit cards or loans, which can lead to debt and financial stress.

To create a cash-based budget, you need to start by identifying all your sources of income, including any rental income or other income sources.

You also need to list all your expenses, including fixed expenses like rent or mortgage payments, utility bills, and loan payments, as well as variable expenses like food, transportation, and entertainment.

Once you have identified your income and expenses, you need to divide your expenses into categories and determine how much cash you need for each category.

You can withdraw cash for each category and use only that cash for the category’s expenses. If you run out of cash in a category, you cannot spend any more money in that category until the next budget cycle.

By tracking your expenses and sticking to a cash-based budget, you can gain greater control over your finances and reduce financial stress. You can also identify areas where you can cut back on spending to save more money or invest in your future.

Remember to review your budget regularly and make adjustments as needed to ensure that you stay on track and achieve your financial goals.

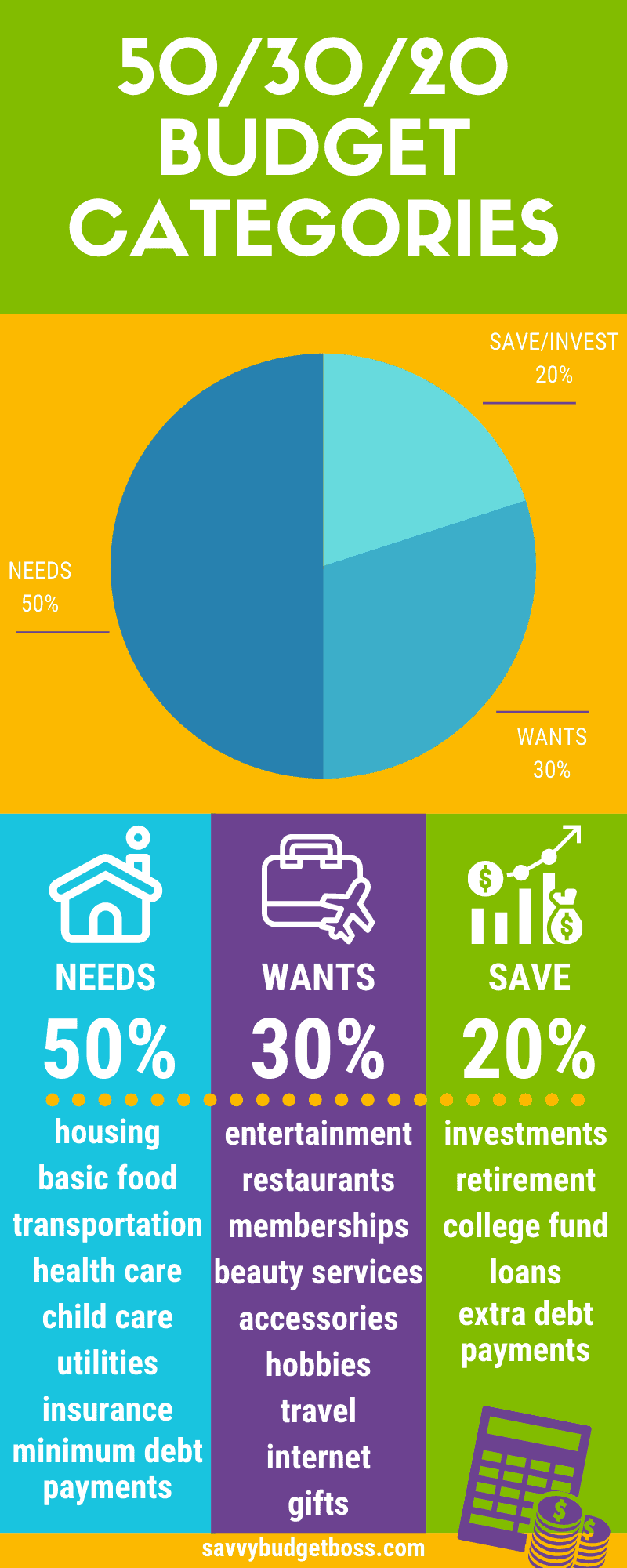

50/30/20 Budget

The 50/30/20 budgeting system was made popular by Senator Elizabeth Warren in her book, All Your Worth: The Ultimate Lifetime Money Plan.

The 50/30/20 budget plan is broken down into the following percentages:

- 50% budgeted for needs: housing, food, transportation, health care, basic clothing, minimum debt payments

- 30% budgeted for wants: entertainment, streaming services, restaurant meals & takeout, accessories, beauty services, gym membership

- 20% budgeted for savings, investments, & (additional) debt payoff: emergency fund, stocks, mutual funds, retirement accounts, extra debt payments

Here’s a free infographic to illustrate the 50/30/20 budgeting method:

30-30-30-10 Budget

The 30/30/30/10 budget is similar to a 50/30/20 budget in that your budget ‘buckets’ are divided up in specific categories.

The budget categories and percentages for the 30 30 30 10 rule are:

- 30% of your take-home income goes towards housing expenses

- 30% goes towards essential expenses

- 30% is allocated to current and future financial goals

- 10% is to be spent as ‘fun money’ or saved for vacations

As you can see, the 30/30/30/10 budget method does not budget as much money for the ‘wants’ category, which may make it a less desirable option for some people.

Bare-Bones Budget

A bare-bones budget is simply budgeting for only your necessary expenses (which have been reduced as far as possible).

A bare-bones budget is a life-saver if you or your spouse has experienced a sudden reduction in pay, or if you’ve recently lost your job.

To create a bare-bones budget, begin by asking yourself the following question: Which of my expenses are vital for survival?

A bare-bones budget only includes the following categories:

- Housing: rent/mortgage

- Utilities: electricity/gas, water/sewer, trash service

- Groceries: does NOT include restaurant meals and take out

- Transportation: to and from work, errands, doctor appointments

- Insurance: home, auto, life, and health

- Health Care: If your income has been cut/eliminated, see if you qualify for state-run insurance.

- Minimum Debt Payments: If possible, continue to make the minimum payments on your mortgage/rent, auto, credit cards/loans, etc.

- Basic Cell or Landline Phone

Any money remaining after filling these budget ‘buckets’ should be used for savings, catching up on past due bills, and paying off outstanding debt.

As you can imagine, a bare-bones budget isn’t very fun. It’s designed to be used during tight financial times. If you find yourself needing to utilize this type of budget for longer than 6 months, you may need to look for additional ways to increase your income.

Envelope Budget

An envelope budget is a simple and effective way to manage your finances. This method involves setting up an envelope for each spending category, such as groceries, entertainment, or transportation, and allocating cash for each category.

Once the envelope is empty, no more spending can occur in that category until the next budget cycle. The envelope budget can help you manage your money by limiting your spending to the cash you have on hand.

You can easily track your expenses and adjust your budget as needed to stay on track. Plus, you can avoid overspending and reduce the temptation to rely on credit cards or loans.

To create an envelope budget, start by identifying your spending categories and how much cash you need for each category. Then, label an envelope for each category and put the allocated cash inside. As you spend money, take cash from the appropriate envelope and track your spending.

By using an envelope budget, you can gain greater control over your finances and reduce financial stress. You can also identify areas where you can cut back on spending to save more money or invest in your future.

Pay Yourself First Budget

The pay yourself first budget is a method that emphasizes saving and investing for your financial goals before allocating money to your expenses. This method involves setting aside a portion of your income for savings and investments, such as a retirement account or emergency fund, before allocating the remaining funds to your expenses.

The pay yourself first budget can help you prioritize your financial goals and ensure that you are saving enough money for your future. By paying yourself first, you can reduce the temptation to overspend and ensure that you have enough money to achieve your financial goals.

To create a pay yourself first budget, start by identifying your financial goals and how much money you need to achieve them. Then, set aside a portion of your income for savings and investments before allocating the remaining funds to your expenses.

By using a pay yourself first budget, you can create a strong foundation for your financial future and achieve your long-term goals. You can also reduce financial stress and gain greater control over your finances.

Remember to review your budget regularly and adjust your savings goals as needed to ensure that you stay on track.

Budgeting Tools

As I said before, there’s no ‘right’ way to budget. You may want to try out a few different budgeting tools and see what works for you.

Pen & paper

My personal favorite way to budget is with a good, old-fashioned pen/pencil and paper. A pencil and paper budget is by far the easiest way to get up close and personal with your budget.

Best of all, it’s FREE!

If you opt for creating a budget with a pencil and paper, you’ll want to pick up a good desktop calculator.

Here are some free printable budget templates to get you started!

Spreadsheets

Microsoft Excel and Google Sheets both offer free budgeting spreadsheet templates. Just plug in your information, and let the template calculate the numbers for you.

Apps

Our phones are always with us, which means our budgets can be too. Budgeting apps make it super convenient to keep track of your spending.

Some popular budgeting apps are:

Budget Planner

A budget planner will help you track your expenses with ease. I use this budget planner, I love that it has pockets for each month so I can keep all of my bills organized.

Here’s a guide to my favorite Budget Planners for 2023

Cash Envelope Wallet

If you’re using the cash envelope system to budget, you’ll quickly learn that carrying all those envelopes around in your purse or pocket can get messy.

This is one of my favorite cash envelope wallets. It’s not too feminine, so it’s perfect for men and women. This cash envelope wallet comes with 12 envelopes and 12 budget sheets, to help you keep your money organized.

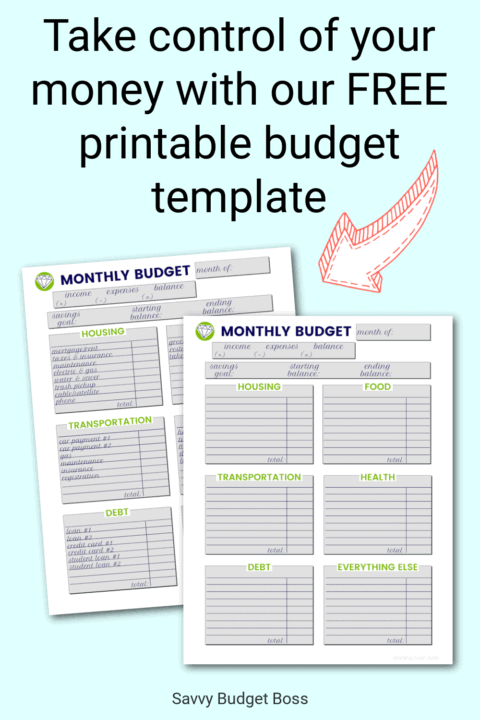

Budget Template (Printable)

If you prefer organizing your budget the old-fashioned way, you’ll love this free printable budget template. It’s designed to be used with a variety of budget methods, such as the zero-sum, 50/30/20, or the bare-bones budget method.

Don’t have a printer? No problem, the text fields are editable, so you can open it with Adobe Acrobat (a free program), type in your amounts, and save it to your computer.

You can snag our free budget template below!

Why Wait? Earn Extra Money Today!

Budgeting Tips for Beginners: Creating a Budget

Hopefully, I can help you learn from my money mistakes by showing you what I believe is the easiest way to create a budget on any income. I say ‘easiest’ because the process of creating a budget is relatively easy (in theory).

However, putting your budget into action and learning to live within your means is often anything but easy.

Grab some paper, a pencil, and a calculator. You could use a handy-dandy electronic device such as a spreadsheet or an app for this step, but for now, we are going to make the budgeting process as easy as possible.

And what could be easier than paper and a pencil?

Once you’ve gotten the hang of budgeting, try out different budgeting methods to find out which budgeting process works best for you.

STEP 1: Determine your monthly income & expenses

Gather up all of your receipts, bills, credit card statements, and bank statements from the previous month. Add up the totals. {I promise, it gets easier from here}!

Next, add up the total take-home income earned for the same month.

This total will include your regular paychecks, money from side jobs, alimony, and child support, social security, retirement, etc.

This total will NOT include money received in the form of gifts, as this type of income is considered extra funds.

Is the total of your income greater than the total of your expenses? If so, great! You’re on the right track. If not, you have two choices:

- Find ways to increase your income. Maybe you could take on a second job, start a blog, sell handmade crafts, take paid surveys, or sell items you no longer use.

- Find ways to decrease your expenses. Look over everything you spent money on last month and see what you can eliminate or reduce. Hint: Start with the grocery budget or try a 30-day no-spend challenge.

Next, divide these items into categories, add up the totals, and write them down.

STEP 2: Itemize and prioritize

What I mean by this is, simply list the most important item of your budget first. Think about what you need to survive; shelter, food, transportation to and from work, clothing, etc.

As such, your mortgage or rent category will be the first line item in your budget. Everything that goes with your housing such as electric/gas, water/sewer, and garbage service will be listed next.

These are your necessary expenses and will need to be paid first each and every month.

Here’s an example of budget categories organized by order of importance:

- Mortgage/Rent

- Electric/Gas

- Water/Sewer/Trash

- Medicine/Toiletries

- Food

- Car Payment(s)

- Fuel

- Auto Insurance

- Phone(s)

- Loan/Debt Payments

- Savings for Future Expenses

- Internet

- Clothing

- Entertainment

*Everyone’s list will be different because everyone’s priorities are different.

For example, you may not have an internet category on your budget if you choose to go without it or if you simply can’t afford it.

Also, you’ll notice clothing is low on the list because I am assuming you have enough clothing (most people do). After all, you probably aren’t reading this post in your underwear!

Plus, clothing (in America at least) is abundant and super cheap if you buy second-hand. Therefore, it is easily attainable.

Let’s talk about the ‘entertainment’ category

The entertainment category will contain everything that is non-essential. Cable or internet TV, cigarettes, alcohol, lottery tickets, eating out, going to the movies, gym memberships, and magazine subscriptions are just some of the items considered extra or ‘entertainment’.

This is where the main differences lie between living on a modest/high-income versus living on a low income.

If you are budgeting for a low income, once you make it to the end of your priority list, you may find you don’t have any money left for entertainment.

You may have to live without this category for a while as you find ways to increase your income, build up savings, and/or pay off debt.

Knowing how to create a budget is one thing…following it is another.

STEP 3: Formulate a plan

Every year, your vehicle(s) registration bill comes in the mail. If you have children in school, they will need school supplies. If you own a car it will need oil changes, brakes, tires, etc. Your kids may want to play an organized sport (or two).

There are birthdays, holidays, and other events to plan for. If you own a home, it will undoubtedly require routine maintenance.

The possibilities for future expenses are endless.

How do you make sure you have room in your budget to handle these non-monthly expenses so they don’t sneak up on you?

The answer is to turn them into monthly expenses. Do your best to calculate how much you spend annually on ‘expected’ expenses. Divide the total by 12 and add that amount to your budget each month.

Do not leave it in your checking account because it has a way of disappearing! Either withdraw the money from the bank and set it aside until needed or transfer it to a savings account.

STEP 4: Build savings

The only way to prevent yourself from going into debt is to set up an emergency fund. Financial expert, Dave Ramsey, recommends an emergency savings of at least $1,000.

If you are trying to create a budget on a low income, $1,000 can feel more like a million dollars.

So, instead of shooting for $1,000, your goal should be to set aside at least $500 in an emergency savings account and add to it as you can. You should only withdraw money from this account in the case of a true emergency.

An unexpected mechanical problem on your car is an emergency. Dinner at TGI Friday’s is not.

The best way to generate some quick cash for an emergency fund is to sell items you have lying around your house or garage. You’d be surprised at some of the items people will snatch up for the right price.

Also, if you are fortunate enough to qualify for a tax refund each year, consider setting aside a lump sum as soon as you receive your reimbursement.

Another {rather painless} way to build up your emergency savings is to bank any extra or unexpected money you receive.

For example, if you get paid weekly, there are four months in every year when you will receive an extra paycheck. If you are paid every other week, you will receive two extra paychecks per year.

Resist the urge to spend that money and build up your savings account instead.

If you are fortunate to earn a pay raise or are gifted money, bank it, don’t blow it. Trust me, one day, you will be glad you did.

STEP 5: Cut yourself some slack

Once you’ve perfected your budget on paper, put it into action.

Don’t expect to get it right the first time, though. You may need to fine-tune your budget more than once in order to find what works and what doesn’t.

You may also need to draft a new budget each month if your income and expenses vary.

If you find yourself consistently going over your budget, you will need to pinpoint the categories you are overspending in and either find ways to cut back or shift money over from other categories in order to make up the difference.

STEP 6: Change your perspective

Once you learn how to create a budget, and stick to it, you will discover a freedom you never thought was possible. Living on a budget is liberating, not restrictive. You will finally be in control of your money instead of it being in control of you.

As you pay off your debt you will free up more breathing room in your budget to save or spend as you see fit.

The most important thing, though, is to be content with your life whether you have a little or a lot. And remember, it’s never too late to improve your financial situation.

How To Budget Irregular Paychecks

Budgeting with an irregular income looks a lot like budgeting with a regular income. You’ll just need to make a few key adjustments going forward.

1. Average your paystubs

Add up the total of your last three pay stubs and divide by (3) in order to find your average pay. Or, you can err on the side of caution and base your budget on your last lowest paycheck.

Then, use this amount to create a bare-bones budget. Once you’ve created a bare-bones budget, you can allocate any remaining funds to the ‘savings’ and ‘wants’ categories.

2. Bank overages to compensate for tight months

Whenever your monthly income exceeds the amount you came up with in step one, save it. Build up an emergency fund of at least $1,000. Once this is done, move on to step 3.

3. Budget a month ahead

Your ultimate goal when budgeting with an irregular income should be to save up a month’s worth of living expenses. This way, you aren’t relying on the current month’s income for that month’s bills.

4. Pay your most expensive (high priority) bills first

Usually, these bills will be your rent/mortgage, followed by auto loans and utilities. Get these bills taken care of as soon as enough money is available. Then, pay your smaller bills in the order they are due.

How To Stick To A Budget

So, you’ve got your budget all made up. It sure does look good on paper, doesn’t it? Now, how do you actually follow a budget?

What happens if you go over? What do you do with extra money that comes along?

Be honest

One key way to ensure you stick to your budget is to be honest with yourself from the start. Make sure to budget for what you actually spend (not what you think you should be spending).

An example of this is if you normally spend $600 a month on groceries, don’t allocate $400 for groceries because that’s how much you wish you were spending. If you do this, you will absolutely blow your budget.

If you do want to cut back in a particular area of your budget, it’s best to plan for small, incremental changes, rather than having an ‘all or nothing approach’.

Know your ‘why’

If you don’t set financial goals to work towards, your budget will likely fail. Failing to set goals is like a runner without a finish line. What’s the point?

Maybe you want to get out of debt, build an emergency fund, or save for a down payment on a house. Whatever your money goals, big or small, keep them in mind as you create your budget. This will help motivate you to keep moving forward with your budget even when you don’t necessarily want to.

Give yourself grace

When it comes to budgeting, practice makes perfect. Expect to fail the first month or two (or three). Everyone does!

Cut yourself some slack and stick to it. I promise, sooner or later, you’ll actually find yourself looking forward to budgeting and you’ll wonder how you ever lived without one.

Change your money mindset

Sometimes, we have to ‘trick’ ourselves in order to achieve an undesirable task. And, let’s face it, most people would not consider budgeting a pleasant task!

If you go into budgeting with a negative mindset…thinking budgets are evil, restrictive, totalitarian documents, YOU WILL FAIL!

Remember, when it comes to creating a budget, you are in complete control!

Rather than choosing to focus on all of the things you cannot do because they are not ‘in the budget’. Find ways to include your favorite activities/purchases (in smaller, more affordable ways) instead.

Of course, no one can have everything! However, living on a budget shouldn’t be an exercise in torture.

If at first, you don’t succeed…

Try something else. Seriously, I am not going to tell you to try the same budgeting method over and over again if it doesn’t work for you.

For example, if you’ve been stressing yourself out over the cash envelope system and have repeatedly tried it and failed, switch to a zero-based budget instead.

You may even find you like some components of one method mixed with parts of another, and this is totally fine!

Also, if spreadsheets aren’t your thing, don’t force yourself to learn excel. Try using a budget planner instead.

Get everyone onboard

When my husband and I first began budgeting, I’ll admit, because I was the one who paid the bills each month, he had no clue how much we made let alone how much money we spent each month.

I wish I could say that creating a budget forced us to start communicating about money, but, unfortunately, that didn’t happen until much later.

We only recently began having monthly ‘money meetings’ and I can only say, I wish we would have done it sooner! We are finally (after 24 years of marriage) getting on the same page when it comes to budgeting our combined income. OMG…what took us so long?

We’ve even started including our two teenage sons in regular budget meetings. They are finally starting to realize money doesn’t actually grow on trees!

Dave Ramsey would be so proud of how we’ve (mostly) stopped making stupid money mistakes!

Pay yourself first

A key way to stay motivated when it comes to sticking to a budget is to pay yourself first. Even if you are living on a tight budget, try to squeeze out a little ‘fun money’ each month.

Your ‘allowance’ can be as little as $10 or up to $100, depending on the amount of wiggle room in your budget.

Take this money out in cash (or transfer to a separate account) and spend it on something special each month. Or, you may choose to save it up over a period of time for larger ‘guilt-free’ purchases.

Beware of common budget-busters

Did you know Christmas falls on the same day each and every year? {Gasp}

Also, there’s a good chance your car will need tires, your kid will need braces, or the washing machine will give out at some point.

There’s even a pretty good chance these things will happen all at once!

Don’t be taken by surprise, plan for common budget-busters before they happen. This is why having an emergency fund is so important.

Learning how to create a budget and subsequently living on it, has its rewards.

Think about it, living on less than you earn will allow you to pay off debt faster, build wealth, and finally be in control of your money!

Envision being content with where you are and with what you have. These budgeting tips for beginners can get you there.

Brian Hebert is a Certified Financial Coach and a graduate of the Villanova University Business School. He specializes in practical debt-elimination strategies, disciplined budgeting, and building long-term financial stability.

Brian’s unique, mission-focused approach to personal finance is rooted in his career in high-stakes, high-discipline roles.

Professional Experience: As a Professional Airline Pilot, a former USAF Fighter and Mobility Pilot, and a Supervisor Air Interdiction Agent with Homeland Security, Brian is an expert in risk mitigation, systematic planning, and disciplined execution. These are the same principles he applies directly to financial success.

Expertise & Certification: He holds a Certified Financial Coach designation and is a graduate of the rigorous Dave Ramsey Financial Coach Masterclass.

Discipline & Trust: Brian’s foundation in discipline is further cemented as a dedicated Martial Arts Practitioner, demonstrating the long-term commitment and systematic practice required for mastery—qualities directly transferable to achieving long-term financial goals. His public service background further reinforces his exceptional level of integrity and commitment.

Brian uses his unique experience in high-accountability environments to help readers treat their financial goals like a mission, providing clear, actionable, and trusted advice.